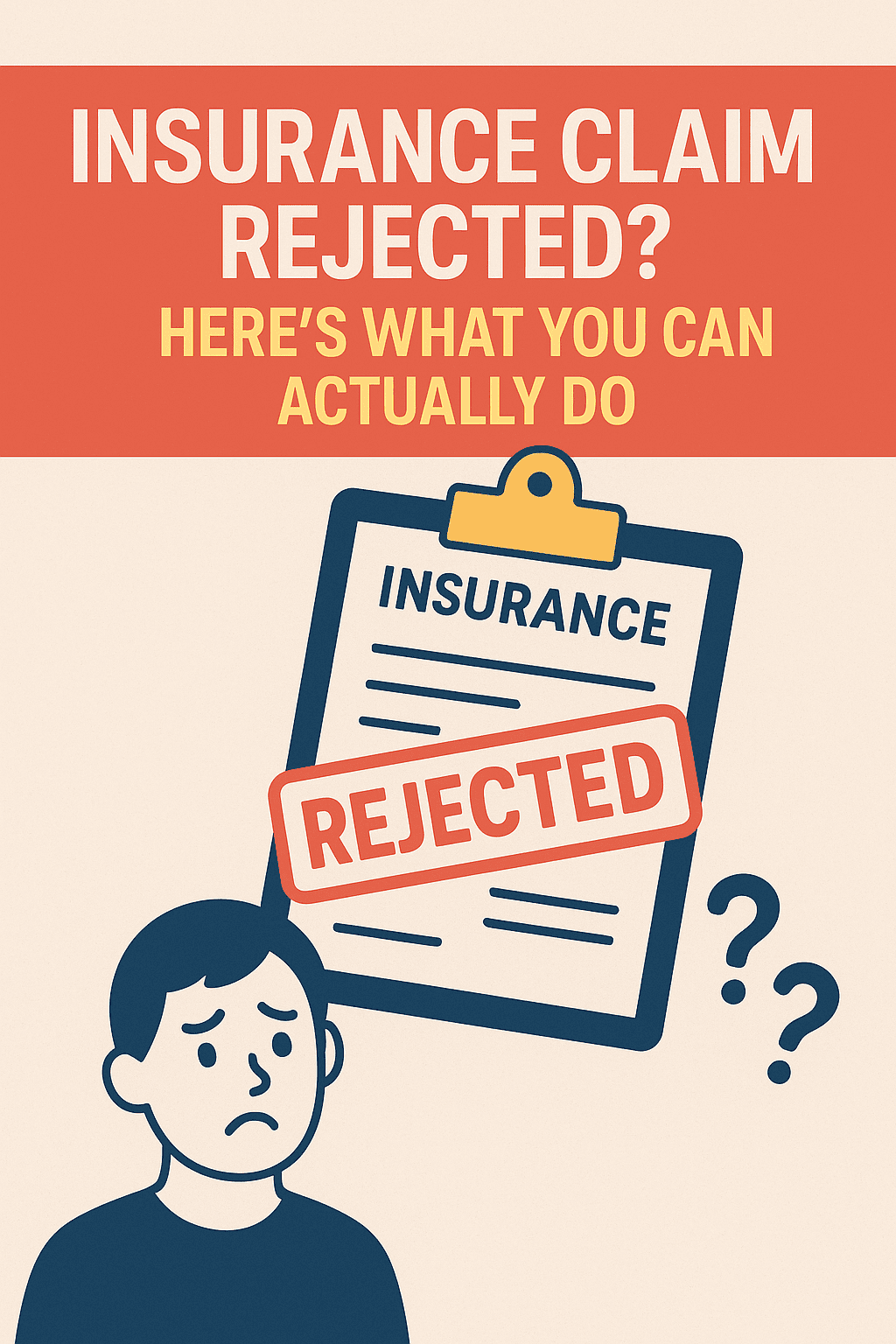

Insurance Claim Rejected? Here’s What You Can Actually Do

Insurance Claim Rejected? Here’s What You Can Actually Do

It always feels like this happens when you least need another problem. Maybe you were already dealing with a hospital bill, a car accident, or something that left you drained — and now, out of nowhere, your insurer says no.

No payout. No clear reason. Just… sorry, your claim’s been rejected.

If you’re in that boat, you’re not alone. It happens more often than people realize. The good news? Rejection isn’t always final — and you do have options. But you have to take the next few steps carefully.

Let’s walk through them — like you’re figuring it out with a friend, not a lawyer.

Step 1: Pause Before You React to claim rejected.

It’s easy to assume the worst — that the insurance company just doesn’t want to pay. Maybe that’s even true. But right now, the most useful thing you can do is get calm and get clear.

Find the rejection letter or email. Read it. Like, really read it. Most people skim it or get stuck on the first sentence. Don’t do that.

They’ll usually mention a clause, a missing document, or a policy term. Highlight whatever reason they give. That’s your starting point.

Step 2: Pull Out What You Sent Them — All of It in claim rejected

Here’s the hard truth: most claims that get denied don’t fail because of fraud or cheating. They fail because something went missing. A signature. A discharge sheet. An invoice that looked “unclear.”

Open the folder or email thread where you stored your documents. Double-check each one. Compare it with what the company’s asking for.

And be honest — did you miss anything? If yes, don’t beat yourself up. Just fix it and get it ready to re-send.

Step 3: Call, Don’t Just Email in claim rejected

This part makes a real difference.

Call the company. Not the agent — the claims department. Ask to speak to someone who handles rejections. Tell them you got the letter, and ask them to explain what exactly went wrong — not in legal terms, but in plain English.

Write down what they say. Dates. Names. Suggestions. The more notes you take, the easier it’ll be if you need to escalate the issue.

Step 4: If You Think They’re Wrong, You Can Fight Back

Let’s say you reviewed everything and you still think your claim was valid — they just found a loophole.

That’s where India’s grievance system comes in.

Every insurer is regulated by IRDAI, and they’re legally required to handle complaints through a formal process. If the company doesn’t resolve your complaint within 15 days, you can go higher — to IRDAI or even the Insurance Ombudsman.

This isn’t a courtroom. It’s meant to protect people like you.

Step 5: Fix What You Can and Reapply

If you realized the mistake was yours — a late document, a missing record — that’s okay. Most insurers allow resubmission.

Write a letter (keep it simple), attach everything again, and send it with your updated paperwork. In many cases, that’s enough to get the claim approved.

Just don’t stay silent. Rejection isn’t the end — it’s just a hurdle.

Real Talk

It’s exhausting. You pay your premiums. You believe you’re covered. And then when you need help, you feel stuck in paperwork and policy terms.

But you’re not powerless.

Ask questions. Challenge vague answers. Push back when something doesn’t make sense. Insurance companies count on most people just giving up. Don’t let that be you.

And if you need help figuring it out, talk to someone who knows this space — like us at Policyzar. We’re not bots. We get it.

Want help with a claim problem?

Reach out at Policyzar.com and myinsurancedost.com — we’ll look at your documents, explain what’s going wrong, and help you make a solid plan to move forward.