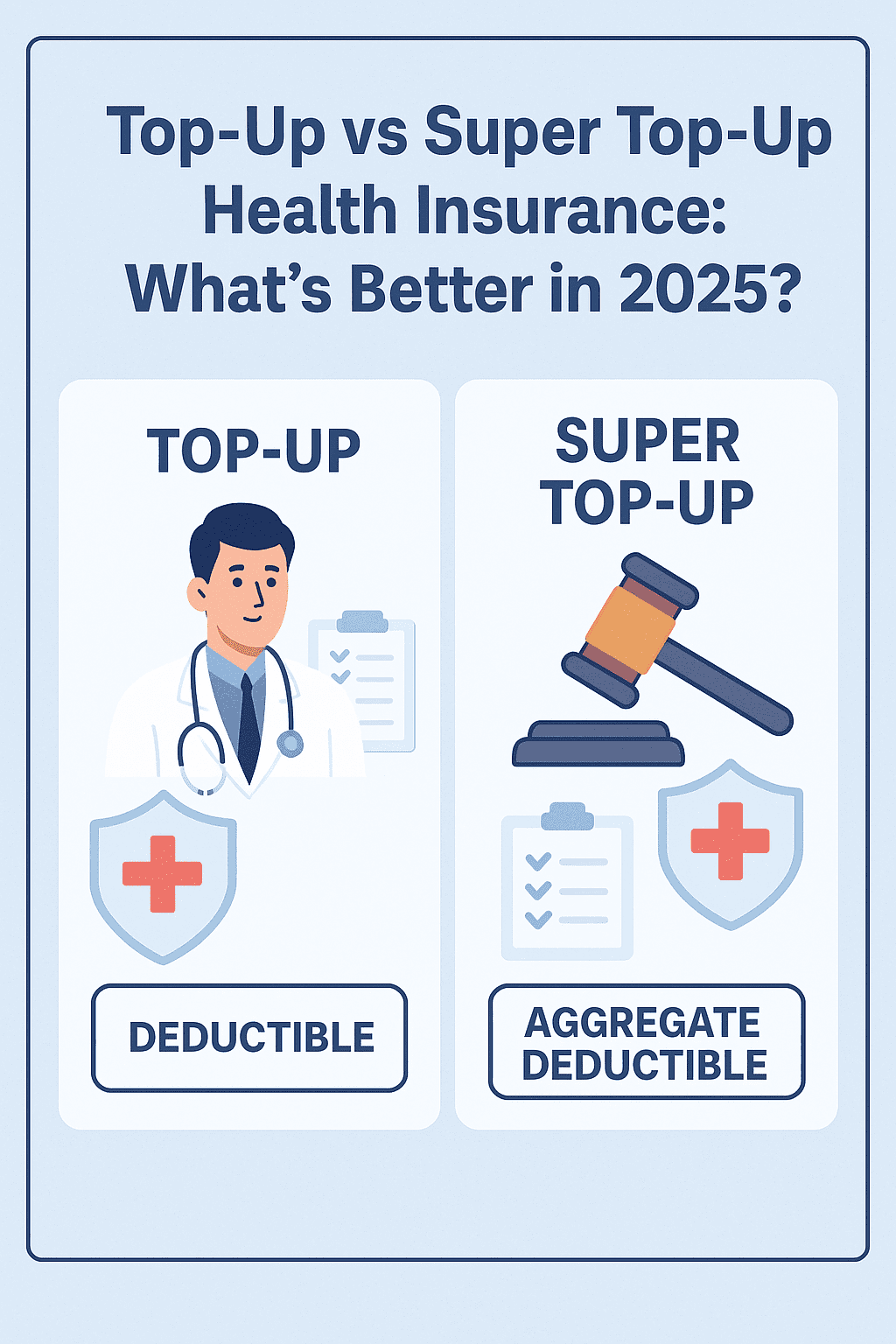

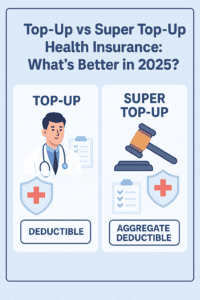

Top-Up vs Super Top-Up Health Insurance: What’s Better in 2025?

Top-Up vs Super Top-Up Health Insurance: What’s Better in 2025?

Don’t Let Medical Bills Surprise You

Let’s be real: medical costs in 2025 are through the roof. Even if you already have a decent health insurance policy, one major hospital visit could still leave you with a shocking out-of-pocket bill. That’s where top-up and super top-up health insurance plans come in.

But let’s be honest — the names sound confusing, right? What’s the actual difference? Which one do you really need? And how do you know if you’re making the smart choice for your family?

Don’t worry. You’re about to find out — in plain, human language.

What Exactly is a Top-Up Health Insurance Plan?

A top-up health insurance plan is like a booster for your existing health coverage. Think of it as a backup parachute — it kicks in only when your hospital bill exceeds a certain amount. This threshold is called the deductible.

Let’s break it down with an example:

You’ve got a top-up plan with ₹10 lakh cover and a ₹5 lakh deductible. If you’re hospitalized and the bill is ₹8 lakh:

- The first ₹5 lakh? That’s on you (or your base health policy, if you have one).

- The remaining ₹3 lakh? That’s where your top-up policy steps in.

But here’s the catch: This applies per claim. So if you have two separate bills of ₹4 lakh each — the top-up plan won’t help. Each bill is below the deductible.

Read more about how top-up health insurance works.

So What is a Super Top-Up Health Insurance Plan?

Glad you asked — because a super top-up is a smarter upgrade.

It also has a deductible like the top-up plan, but instead of applying it to each individual claim, it adds up all your hospital bills throughout the year. If the total medical expenses exceed the deductible, the super top-up plan takes over from there.

Example time again:

Same ₹10 lakh cover, ₹5 lakh deductible.

- First hospitalization: ₹3 lakh

- Second hospitalization: ₹4 lakh

- Total: ₹7 lakh

Now you’re above your ₹5 lakh deductible. So your super top-up plan will pay the remaining ₹2 lakh.

That’s why super top-ups are especially useful for people with recurring health issues or senior family members.

Explore India’s best super top-up plans.

Top-Up vs Super Top-Up: Quick Comparison

| Feature | Top-Up Plan | Super Top-Up Plan |

|---|---|---|

| Deductible Applied On | Every single claim | Total claims in a year |

| Best For | One big hospital bill | Multiple hospital visits |

| Premium | Slightly cheaper | Slightly higher but more useful |

| Great For | Young, healthy people | Families, seniors, or frequent patients |

Which One Should You Choose in 2025?

Here’s the deal — both are good. But one might be better for your situation.

✅ Top-Up is best if:

- You’re young and healthy

- You already have a solid base policy

- You want protection from a big one-time hospital event

✅ Super Top-Up is better if:

- You have kids, parents, or dependents

- You’ve had multiple hospital visits in the past

- You’re planning for long-term care or chronic illness

Why Adding a Top-Up or Super Top-Up is a Smart Financial Move

Even if you already have a base health insurance policy from your employer or privately — that might not be enough anymore.

Hospital costs are rising. A single ICU stay could easily burn through ₹5 lakh. Instead of upgrading your entire base policy (which can get expensive), just layer on a top-up or super top-up plan.

You’ll get:

- More coverage for less money

- Better preparedness for big health surprises

- Peace of mind for the entire family

Want to check your health insurance gap? Use our coverage calculator.

How Much Cover Should You Actually Go For?

Let’s keep it simple.

🧾 In 2025, medical inflation is around 12–20%.

That means a ₹5 lakh policy that seemed decent five years ago might not cover much today.

Here’s a basic guide:

- Base policy: ₹5–10 lakh

- Top-Up or Super Top-Up: Add ₹10–20 lakh

- Deductible: Match your base plan (usually ₹5 lakh)

And if you’re insuring parents, go even higher. You’ll thank yourself later.

Real Life Scenarios — Which Plan Helped Who?

Ritu, 32, from Bangalore:

“My company gave me ₹3 lakh health cover. I bought a ₹10 lakh super top-up with ₹5 lakh deductible. I ended up using it for my delivery and postnatal treatment. Total peace of mind.”

Sanjeev, 45, from Pune:

“Had a bypass surgery. My base ₹5 lakh policy helped, but the top-up saved me another ₹6 lakh. All cashless. I didn’t even feel the financial hit.”

Neha, 29, from Noida:

“I didn’t think I needed more insurance. But after two gallbladder procedures in a year, my super top-up saved me ₹3.5 lakh. Totally worth it.”

Learn how Policyzar helped thousands choose better coverage.

Why Choose Policyzar for Your Top-Up Needs?

Policyzar isn’t just another comparison website. It’s built for people who want insurance without the jargon.

With Policyzar, you get:

- Instant comparison of top-up & super top-up plans

- All plans from IRDAI-approved insurers

- Support in Hindi, English & more

- No hidden charges, ever

- Real human help if you get stuck

And you can buy, manage, and even renew your plan — all in under 2 minutes.

Or just WhatsApp “TOPUP” to get help instantly.

Quick FAQs — Because You Probably Have Questions

Do I need a base policy before buying a top-up?

Yes. The deductible must be covered either by your employer’s insurance or your personal policy.

Can I use both top-up and super top-up together?

Technically yes, but most people pick one. Super top-up is more flexible.

Is it cashless?

Yes, just like your base plan — provided your hospital is in-network.

Can I buy this online without any agent?

Absolutely. That’s the whole point of Policyzar — no pressure, no paperwork.

Final Thoughts: Protect Your Future — Without Stress

Health emergencies don’t wait for the “right time.” If anything, they come when you least expect them — and usually when your finances are already tight.

That’s why adding a top-up or super top-up to your current health plan is one of the smartest things you can do in 2025.

It’s budget-friendly. It’s flexible. And it’s peace of mind that grows with you.

Take just 2 minutes to compare plans on Policyzar.com. Seriously — it’s faster than ordering food or choosing a Netflix show.

You’ll thank yourself later.

Visit policyzar.com and myinsurancedost.com