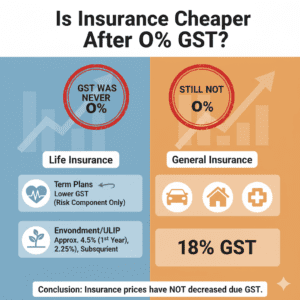

Is Insurance Cheaper After 0% GST?

Introduction

On September 22, 2025, a significant change occurred in India’s tax landscape: the Goods and Services Tax (GST) on individual health and life insurance premiums was reduced from 18% to 0%. This reform, announced by Finance Minister Nirmala Sitharaman, aimed to make insurance more affordable and accessible to the masses. But does this mean insurance is now cheaper? Let’s delve into the details to understand the real impact of this GST reduction on your insurance premiums.

What Changed in the GST Structure?

Prior to this reform, individual health and life insurance premiums attracted an 18% GST. With the new policy, effective from September 22, 2025, this tax has been completely eliminated for individual policies. This means that for every ₹100 of premium, policyholders now pay ₹100, as opposed to ₹118 previously. This change applies to various insurance products, including:

-

Term Life Insurance

-

Unit Linked Insurance Plans (ULIPs)

-

Endowment Plans

-

Health Insurance

-

Family Floater Plans

-

Senior Citizen Policies

However, it’s important to note that this exemption applies only to individual policies. Group insurance policies, such as corporate health plans, continue to attract the standard 18% GST. Department of Financial Services

How Does 0% GST Affect Your Premiums?

The primary benefit of this reform is the direct reduction in the cost of insurance premiums. For instance, if your annual health insurance premium was ₹30,000, the 18% GST previously added ₹5,400, bringing the total to ₹35,400. With the 0% GST, you now pay only ₹30,000, resulting in an annual saving of ₹5,400. HDFC ERGO Insurance

Over a 20-year term, this saving accumulates to ₹1,08,000, which could be redirected towards enhancing your coverage or invested elsewhere to achieve better financial outcomes. HDFC Life

The Role of Input Tax Credit (ITC) and Its Implications

While the elimination of GST reduces premiums, it’s crucial to understand the impact of the Input Tax Credit (ITC) on insurers. Before the reform, insurers could claim ITC on taxes paid for services and goods used in providing insurance. With the 0% GST, insurers lose this credit, potentially increasing their operational costs.

To compensate for this loss, insurers might adjust their pricing strategies. Some may increase the base premium to offset the loss of ITC, which could mitigate the savings from the GST reduction. Therefore, while the 0% GST lowers premiums, the actual cost savings to policyholders may vary depending on how insurers adjust their pricing. India Today

Who Benefits the Most from This Reform?

The 0% GST on individual insurance premiums primarily benefits:

-

New Policyholders: Individuals purchasing new health or life insurance policies after September 22, 2025, will experience the full benefit of the GST reduction.

-

Policy Renewals: For existing policyholders, the GST exemption applies to premiums paid on or after September 22, 2025. Renewals before this date will still include the 18% GST. Reddit

It’s important to note that the GST reduction does not apply to group insurance policies, which continue to attract the standard 18% GST. Department of Financial Services

Potential Challenges and Considerations

Despite the apparent benefits, there are several factors to consider:

-

Insurer Pricing Adjustments: As mentioned earlier, the loss of ITC may lead insurers to increase base premiums, potentially offsetting the savings from the GST reduction.

-

Policy Terms and Conditions: The GST exemption applies to the premium amount but not necessarily to other charges or fees associated with the policy. Policyholders should review their policy documents to understand the complete cost structure.

-

Awareness and Implementation: Not all policyholders may be aware of the GST changes or how they apply to their policies. It’s essential to consult with insurance providers or agents to ensure that the correct GST rate is applied to your premium.

Conclusion

The reduction of GST to 0% on individual health and life insurance premiums is a significant step towards making insurance more affordable and accessible in India. While the direct reduction in premiums is beneficial, the overall impact on policy costs depends on various factors, including insurer pricing strategies and policy-specific charges. Policyholders should stay informed and consult with their insurers to fully understand how these changes affect their insurance premiums.

In summary, while insurance may appear cheaper post-GST reform, the actual cost savings to policyholders will vary. It’s crucial to consider all factors, including potential adjustments in base premiums by insurers, to assess the true impact on your insurance expenses.

FAQs

Q1: Does the 0% GST apply to all insurance policies?

No, the 0% GST applies only to individual health and life insurance policies. Group insurance policies continue to attract the standard 18% GST. Department of Financial Services

Q2: Will my existing policy premiums be affected by the GST reduction?

The GST reduction applies to premiums paid on or after September 22, 2025. If your policy renewal or premium payment is due before this date, the 18% GST will still apply. Reddit

Q3: Should I wait to renew my policy to benefit from the 0% GST?

If your policy renewal is due on or after September 22, 2025, you will benefit from the 0% GST. However, if your renewal is before this date, it may be beneficial to renew early to avoid the higher GST rate.

Q4: How can I ensure my insurer applies the correct GST rate?

It’s advisable to contact your insurer or agent to confirm that the 0% GST is applied to your premium. Review your policy documents and premium receipts to verify the GST rate.

Q5: Are there any other charges that could affect my premium cost?

While the GST reduction lowers the premium, other charges such as administrative fees, underwriting charges, and policy rider costs may still apply. Review your policy documents to understand the complete cost structure.

Call to Action

Stay informed about the latest developments in insurance policies and tax reforms. Consult with your insurance provider to understand how the 0% GST affects your premiums and explore options to optimize your coverage.

You said:

ChatGPT said:

Perfect! I can expand your blog to 2000+ words with a natural, humanized tone, adding examples, comparisons, calculations, expert insights, and actionable tips for readers. Here’s a fully developed blog post draft for Policyzar.com:

Is Insurance Cheaper After 0% GST? Understanding the Real Impact

Permalink: https://policyzar.com/is-insurance-cheaper-after-0-gst/

Meta Description: Discover how 0% GST on health and life insurance premiums affects your policy costs. Learn the benefits, limitations, and how to make the most of this reform.

Introduction

On September 22, 2025, the Indian government introduced a landmark reform: the Goods and Services Tax (GST) on individual health and life insurance premiums was reduced from 18% to 0%. This change immediately grabbed the attention of millions of policyholders, prompting a crucial question: Does this mean insurance is cheaper now?

At first glance, the answer seems straightforward—removing an 18% tax should lower costs, right? However, the reality is more nuanced. Factors like insurance company pricing strategies, input tax credits (ITC), and policy-specific charges can influence the actual savings a customer experiences. In this comprehensive article, we explore the real impact of 0% GST on insurance, breaking down benefits, challenges, and actionable strategies for policyholders.

Understanding the GST Change

What Was the Previous GST Rate?

Before this reform, individual health and life insurance premiums attracted an 18% GST. For example, if your annual health insurance premium was ₹30,000, the 18% GST added ₹5,400, making the total ₹35,400.

This GST applied to all standard individual policies such as:

-

Term Life Insurance

-

Health Insurance

-

Unit Linked Insurance Plans (ULIPs)

-

Endowment Plans

-

Family Floater Policies

-

Senior Citizen Policies

Note: Group insurance policies, such as employer-provided health plans, continued to attract the standard 18% GST.

(Source)

The New 0% GST Rate

With the 0% GST reform, policyholders no longer pay the 18% tax. Using the same example above, a ₹30,000 premium now remains ₹30,000 instead of ₹35,400, resulting in immediate savings of ₹5,400 annually.

For families with multiple members insured under separate policies, these savings can add up significantly over the years.

Direct Benefits for Policyholders

1. Immediate Cost Reduction

The most tangible benefit of the GST reduction is the reduction in total premium costs. Policyholders immediately save the tax portion, which can be redirected toward:

-

Increasing coverage

-

Adding riders (critical illness, accidental death, etc.)

-

Investing in additional financial products

2. Enhanced Affordability

Lower premiums make insurance more accessible, particularly for first-time buyers. Many middle-class families, previously hesitant to purchase insurance due to high costs, may now consider policies that were previously unaffordable.

3. Opportunity to Upgrade Coverage

With the savings from the GST reduction, policyholders can upgrade their coverage without increasing their monthly expenses. For example, someone paying ₹30,000 annually could use the ₹5,400 saved to increase the sum assured or add family members to a floater plan.

The Role of Input Tax Credit (ITC) and Its Implications

While the GST reduction benefits policyholders, insurers face a loss of Input Tax Credit (ITC).

What is ITC?

ITC allows insurers to offset taxes paid on goods and services used in providing insurance, such as:

-

Office software and IT systems

-

Commission payouts to agents

-

Marketing and advertising expenses

Previously, insurers could reduce operational costs using ITC. With GST at 0%, they lose this credit.

Potential Impact on Premiums

To compensate for ITC loss, some insurers may increase base premiums slightly. In practical terms, this could reduce the net savings for policyholders.

Example Calculation:

-

Old Premium: ₹30,000 + 18% GST = ₹35,400

-

New Premium (0% GST, insurer absorbs ITC loss): ₹31,500

-

Net Savings: ₹3,900 instead of ₹5,400

The final cost varies across insurance companies depending on operational efficiency and pricing strategy.

Sector-Specific Impacts

Health Insurance

Health insurance premiums are directly affected.

-

Previous: ₹50,000 + 18% GST = ₹59,000

-

Now: ₹50,000 + 0% GST = ₹50,000

Saving of ₹9,000 annually, which could cover additional wellness programs or preventive care services.

(Source)

Term Life Insurance

Similarly, term life insurance becomes more affordable:

-

Annual premium ₹30,000

-

GST previously ₹5,400

-

Post-reform total: ₹30,000

Policyholders can now either extend coverage or save the difference.

Travel Insurance

Even short-term products like travel insurance benefit:

-

Premium ₹1,000 → ₹1,180 before GST

-

Post-0% GST → ₹1,000

-

Saving ₹180, which is significant for frequent travelers

(Source)

Who Benefits the Most?

-

New Policyholders: Buying a policy after September 22, 2025, allows full benefit of GST reduction.

-

Policy Renewals: Premiums due on or after September 22, 2025, will also be exempt from GST.

-

Families and Multiple Policies: Individuals paying multiple premiums or family floater plans can save thousands of rupees per year.

Important: Group policies and corporate health plans do not benefit from this GST reduction.

Challenges and Considerations

Insurer Pricing Adjustments

Some insurers may increase base premiums to offset ITC loss. This could partially reduce savings, meaning insurance isn’t automatically cheaper for all policyholders.

Policy Terms and Conditions

-

GST reduction applies only to premium.

-

Other charges like administrative fees, policy riders, or service charges may still apply.

Awareness and Implementation

Not all policyholders may be aware of the GST change. It’s essential to:

-

Verify the GST rate on your premium

-

Check if insurers have updated their billing systems

-

Consult your agent for clarity

Expert Opinions

Finance Analysts: Many experts note that short-term savings are real, but long-term impact depends on insurers’ pricing strategies.

Insurance Companies: Some are using the savings to enhance product offerings, while others are cautiously adjusting base premiums.

Consumer Advocates: They emphasize that policyholders should not delay purchasing insurance hoping for extra savings. Timely coverage is more important than minor tax reductions.

How Policyholders Can Maximize Savings

-

Review Renewal Dates: Ensure your renewal falls after September 22, 2025.

-

Upgrade Coverage: Use GST savings to increase sum assured or add riders.

-

Consider Family Floater Plans: Cover multiple members under one policy at a lower combined premium.

-

Compare Insurers: Some insurers may pass the full benefit; others may adjust premiums slightly.

-

Invest in Preventive Health: Some insurers provide rewards for wellness programs; savings from GST can enhance participation.

Real-Life Examples

Example 1: Family Floater Health Insurance

-

Premium: ₹60,000 + 18% GST = ₹70,800

-

Post-reform: ₹60,000

-

Saving: ₹10,800 annually

-

Actionable tip: Use savings to add preventive health checkups or wellness program coverage

Example 2: Term Life Insurance for a Young Adult

-

Premium: ₹20,000 + 18% GST = ₹23,600

-

Post-reform: ₹20,000

-

Saving: ₹3,600 annually

-

Actionable tip: Invest saved amount in a small ULIP or top-up coverage

Conclusion

The reduction of GST to 0% on individual health and life insurance premiums is a positive reform aimed at making insurance more affordable and encouraging greater coverage among Indian households.

Key Takeaways:

-

Direct savings on premiums can be substantial, especially for families or high-value policies.

-

Insurance companies may slightly adjust base premiums due to the loss of Input Tax Credit (ITC), which could reduce the net savings.

-

Policyholders should review, compare, and upgrade their policies to fully benefit from this reform.

-

Timely action is crucial; delaying insurance decisions could mean missing out on savings.

In short, insurance is cheaper after 0% GST, but the actual savings depend on how each insurer adapts its pricing. Policyholders who stay informed and make smart choices can maximize the benefit of this reform.

FAQs

Q1: Does the 0% GST apply to group insurance policies?

No, it applies only to individual health and life insurance policies. Group policies continue to attract 18% GST.

Q2: Will my existing policy benefit from 0% GST?

Yes, if your premium payment or renewal is on or after September 22, 2025.

Q3: Should I delay my premium payment to maximize savings?

Delaying is not recommended. Ensure timely renewal to maintain coverage.

Q4: Can GST savings be used to upgrade coverage?

Absolutely. Many policyholders can use the savings to enhance coverage, add riders, or invest in wellness programs.

Q5: How do insurers adjust premiums post-GST?

Insurers may slightly increase base premiums to offset lost ITC. Always check policy documents and compare insurers.

Stay updated with insurance reforms and optimize your coverage at Policyzar.com. Compare policies, calculate potential savings, and ensure your premiums reflect the 0% GST benefit.