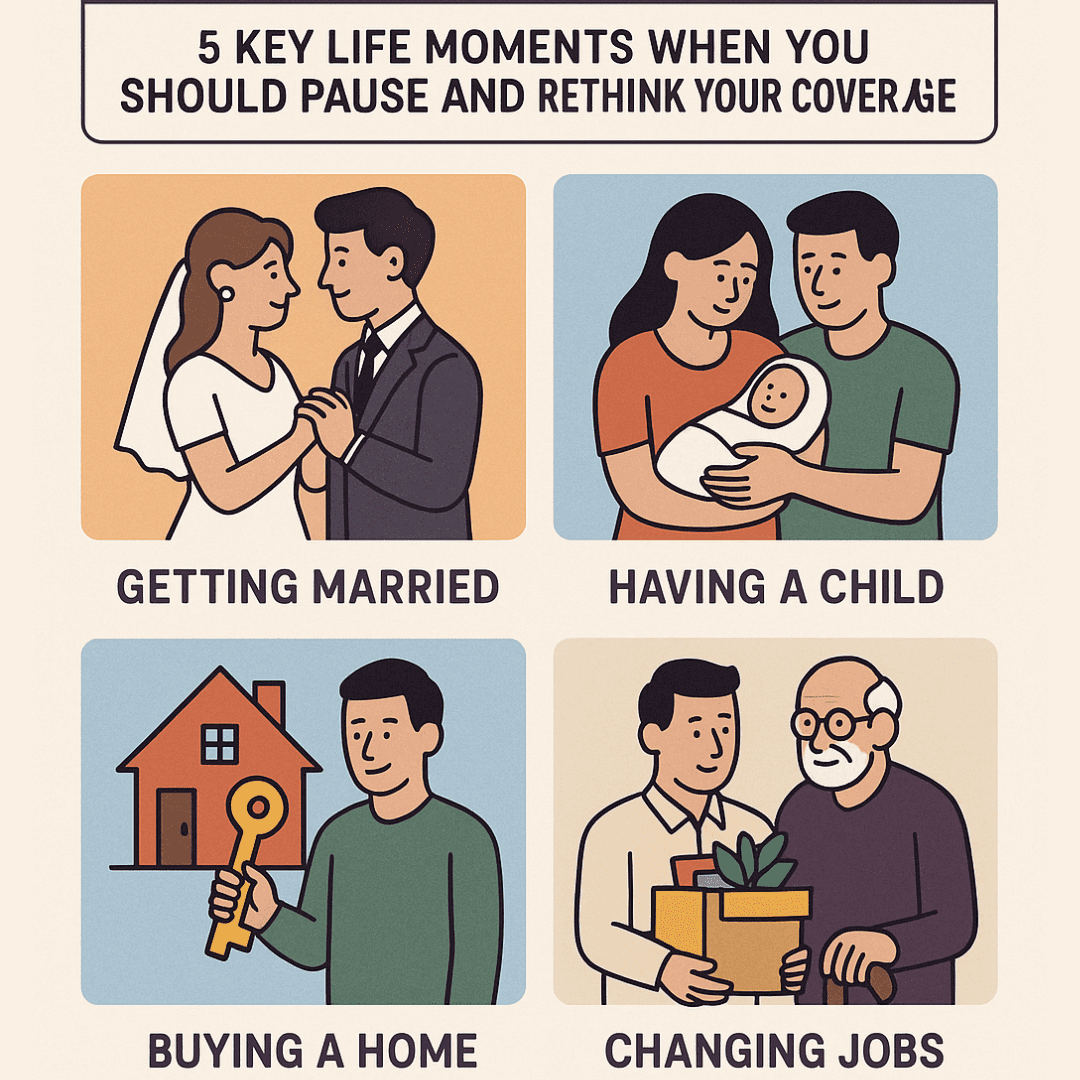

Review Your Insurance Plan: 5 Key Life Moments When You Should Pause and Rethink Your Coverage

Review Your Insurance Plan: 5 Life Moments That Deserve a Rethink

Let’s face it—buying insurance usually feels like a one-time chore. You spend a few hours comparing plans, pay the premium, tuck the policy away in a drawer… and forget about it.

But here’s the truth: your life changes, and when it does, your insurance should too.

Whether you’re getting married, having a baby, switching jobs, or going through a health scare—each major milestone deserves a pause and a quick review of your insurance plan. It’s not about spending more. It’s about making sure you’re protected the right way, at the right time.

So, let’s break it down. Here are five key life moments when you should hit the pause button, take a breath, and ask: “Does my insurance still have my back?”

Review your insurance plan 1. Just Married? Time to Think Like a Team

Marriage isn’t just about sharing Netflix passwords—it’s about sharing dreams, goals, and yes, financial responsibilities.

Why it matters:

You’re now building a future together. If something were to happen to either of you, it affects both.

Things to check:

- Update your nominee: If you already had a policy, make sure your spouse is now the beneficiary.

- Bump up your term insurance: Your spouse may now depend on your income. Cover that risk.

- Combine your health plans: A family floater plan often saves money and offers better coverage than two individual ones.

True story:

When Rahul and Sneha from Pune got married, they merged their individual health plans into one floater policy. Result? Higher coverage and 15% less in annual premiums.

Tip: Don’t blindly trust employer-provided insurance. It disappears the day you switch jobs.

Keywords: life insurance after marriage, family health insurance plans, updating nominee after marriage

Review your insurance plan 2. Baby on the Way? Your Insurance Needs Just Doubled

Few things change your life as quickly—and beautifully—as becoming a parent. With that new little heartbeat comes a mountain of love… and lifelong responsibility.

Time to rethink:

- Your life insurance: Make sure your term plan covers your child’s future needs, from school fees to college dreams.

- Health insurance: Add your baby to your plan. Some policies allow this from Day 1, others after 90 days.

- Start a savings plan: Child ULIPs, PPF, Sukanya Samriddhi (for girls), and even SIPs work well.

Real talk:

Arun from Hyderabad increased his term cover from ₹50 lakh to ₹1.5 crore after his son was born. He also started a SIP of ₹5,000/month with a 15-year goal for education.

Bonus Tip: Use online calculators to forecast college fees in 15–20 years. You’ll thank yourself later.

Keywords: baby health insurance, term plan for parents, child education insurance India

Review your insurance plan 3. Buying a Home? Protect That Dream

Buying your first home is exciting—but it also means years of EMIs. What happens to your family if something happens to you?

Make sure your insurance steps in:

- Top-up your term plan: Your life cover should at least equal your home loan.

- Consider a mortgage-reducing plan: These shrink over time, just like your loan.

- Avoid bundled bank insurance: They’re often expensive, full of fine print, and non-transferable.

Did you know?

As of 2025, average home loans in urban India hover around ₹35–40 lakh. That’s a huge liability for your loved ones if you’re not around.

Real example:

Sonal took a ₹50 lakh home loan in Delhi. She added a top-up of ₹60 lakh to her term plan instead of taking the bank’s offer. She saved ₹18,000 in premiums per year—and got better flexibility.

Pro Tip: Use PolicyZar’s loan calculator to find the exact cover you need.

Keywords: mortgage insurance India, term plan for home loan, home buyer insurance India

Review your insurance plan 4. New Job? Bigger Salary? Time to Level Up

Congrats on the new job or raise! But while your paycheck has grown, your insurance plan from five years ago might still be stuck in the past.

Here’s what to check:

- Update your term life cover: Ideally, it should be 10–15x your current income.

- Review your health plan: Relying only on employer-provided coverage? Risky move.

- Recheck old investments: That endowment plan from 2010 might not fit your goals anymore.

Example:

After joining an MNC, Priya upgraded her health insurance to ₹20 lakh and increased her life cover from ₹30 lakh to ₹1 crore. She also shifted her savings from a traditional plan to a diversified mutual fund SIP.

Smart move: Keep a personal health plan that stays with you—even if your job doesn’t.

Keywords: insurance after promotion, salary hike insurance check, personal vs group health plan

Review your insurance plan 5. Health Scare in the Family? Wake-Up Call Alert

It’s sad but true—most people only think about insurance when a medical emergency hits. Don’t wait for a wake-up call.

What to do right now:

- Add a critical illness rider: Covers cancer, heart attacks, strokes, and other serious conditions.

- Boost your health cover: Medical inflation is real. A single ICU visit can wipe out ₹5–10 lakh.

- Add a super top-up: High coverage, low premium—especially useful for families or seniors.

- Cover your parents too: Look for senior citizen policies with high sum insured and no co-pay.

Real story:

Anjali’s mother was hospitalized after a stroke. Their ₹3 lakh policy was exhausted in 3 days. That’s when she realized: “You never think it’ll happen—until it does.” She now has a ₹20 lakh cover with a ₹30 lakh top-up for both parents.

Fact: Private hospital bills rose by 12–18% last year. Plan accordingly.

Keywords: critical illness insurance India, super top-up plans, health cover for parents

Review Your Insurance Plan Bonus Moments You Shouldn’t Ignore

Apart from the big five, these life changes should also trigger an insurance review:

- Moving abroad (NRIs need specific plans)

- Starting your own business

- Divorce or separation

- Retiring from your job

- Major illness recovery

Quick Example:

When Mehul quit his job to freelance, he had to buy both life and health plans from scratch—no more employer backup. Luckily, he planned ahead.

Final Thoughts: Insurance Isn’t Set-and-Forget

You don’t need to stress about insurance every day. But every year—or every time your life takes a new turn—it’s worth asking:

“If something changed tomorrow, would my insurance still work for me?”

It only takes 15 minutes to review your plans. And it can save your family from years of financial stress.

Here’s your cheat sheet:

- After marriage

- After having a baby

- After buying a home

- After a job switch or salary hike

- After a family health scare

- When starting a business

- Before moving abroad

- Before retiring

Insurance plan check FAQs (Friendly & Straightforward)

Q. How often should I review my insurance?

A. Once a year—or whenever your life changes significantly.

Q. Can I hold multiple policies?

A. Totally. Just make sure each one serves a purpose, and premiums fit your budget.

Q. Is it worth upgrading an old term policy?

A. Yes, especially if your income or dependents have grown. Check with your insurer for upgrade options.

Q. What’s better—floater or individual health insurance?

A. Floaters are great for couples and young families. But for elderly parents, individual plans may work better.

Q. Where do I start if I’m overwhelmed?

A. Use platforms like PolicyZar.com or MyInsuranceDost.com for easy comparisons and expert guidance.

Final Word: Insurance is Self-Care

Protecting your family’s future is one of the most loving things you can do. So take a moment, review your coverage, and make sure you’re not just insured—but properly protected.

Because life changes. And when it does, your insurance should keep up.

Don’t late just visit policyzar.com and myinsurancedost.com to secure your future.